The study was prepared with the support of the German Economic Team in Ukraine (GET).

How to restrict abuse of the simplified tax system

Business

| 3 November 2021

In order to promote the growth of small and medium enterprises (SMEs) and to induce them to operate in the formal sector of the economy, Ukraine operates a Simplified System of Taxation (STS) for SMEs alongside its regular business taxation regime. While the STS clearly contributes to reduce administrative and tax burdens on SMEs, it is known that the system is being abused by companies illegally underreporting their revenues or semi-legally splitting revenues into different companies.

This paper is analysing the extent of revenue underreporting in groups 1-3 of the STS and provides policy recommendations on how to combat it. Revenue underreporting allows companies to reduce their tax burden by permitting them to stay either in groups 1 or 2 of the STS, in which only a small lump-sum tax is paid, to benefit from the still relatively low turnover tax in group 3 of the STS, or to simply pay less proportional tax by underreporting the tax base. It creates fiscal losses to the state, but also gives tax abusers an unfair competitive advantage against compliant companies.

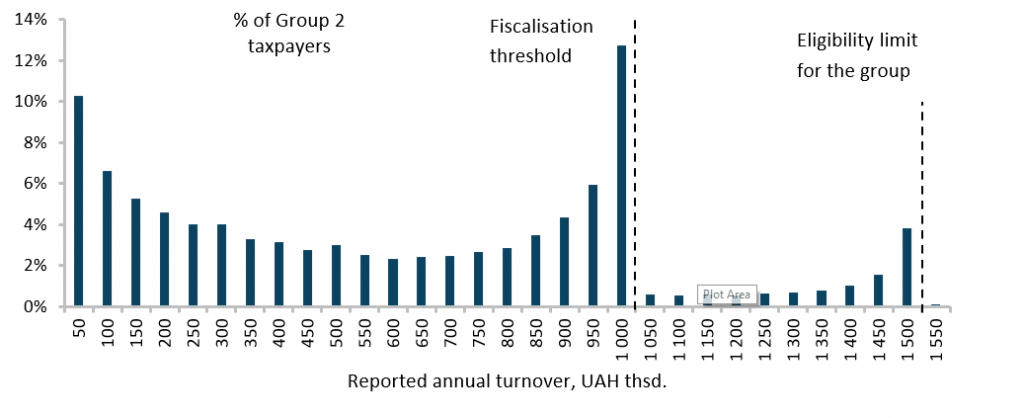

Analysing the distributions of taxpayers by turnover in groups 1-3 of the STS, we find most evidence of underreporting in group 2. Whilst the distribution of taxpayers should theoretically be a convex decreasing function, we find sharp spikes (bunching up) of taxpayers between two important thresholds: The current fiscalisation threshold after which the use of an electronic cash register is compulsory and the maximum turnover limit for the group.

Distribution of taxpayers by turnover, group 2

Source: State Tax Service in Ukraine 2019 data, CES calculations

As group 2 is the last group with a lump-sum taxation, this indicates that many companies attempt to “hide” in this group to evade a much higher tax burden based on proportional taxation of their true turnover in group 3. Distributions in groups 1 and 3 are relatively close to the theoretical distribution and hence present much less indication of turnover underreporting. Within group 2, the activities that exhibit the most indications of turnover underreporting combined with large economic size are retail trade, the Gastronomy (HoReCa = Hotels, restaurants, cafes) sector and manufacturing companies. In the case of retail trade companies under group 2, it is likely that the fiscal losses created by them are not only stemming from underreporting under the STS but also from the sale of ‘grey’ smuggled imports on which no customs duties or import VAT has been paid. Customs related losses are estimated at up to UAH 96 bn per year.

In order to reduce the fiscal losses and discrimination against compliant companies resulting from turnover underreporting in the STS, we recommend three measures:

- A refocusing of groups 1 and 2 on the smallest of businesses in specific activities: As the lump-sum tax regime is in principle intended only for micro-businesses in areas not suitable for proportional taxation, it should be refocused on this. Activities should be restricted to small-scale personal services, micro businesses in gastronomy and sale of homemade, artisanal or agricultural products. Exact criteria should be carefully designed in order to exclude possible loopholes for abuse, but turnover limits should be set wide enough such that all genuine micro businesses fitting the activity criteria can fit into these groups.

- Full fiscalisation of group 3 of the STS: Full fiscalisation of the entities under the STS (except in group 1) is already enshrined in law, but implementation of the requirement has been postponed. In order to ensure that businesses in group 3 of the STS cannot so easily conceal cash incomes, it is imperative that fiscalisation is fully implemented and no further delays are granted

Introduction of compulsory VAT on for retail businesses in group 3 of the STS: In order to combat the large problem of the sale of smuggled goods by retail companies, it is necessary that trade companies must document their purchases of goods in a traceable manner. Compulsory participation in the VAT will achieve this whilst requiring only a manageable administrative burden as documentation of VAT expenditures by businesses is not too difficult and practiced successfully in many other areas of the Ukrainian economy.

Explore more